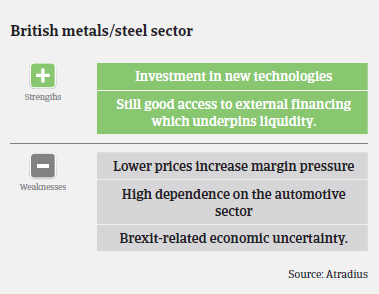

Domestic metals and steel demand is increasingly affected by subdued investment in the construction sector and a marked demand slowdown from automotive.

- Insolvencies expected to increase 5% in 2020

- Payments take 60 days on average

- Ongoing consolidation process

The UK domestic metals and steel demand situation has remained rather stable so far, but is increasingly affected by subdued investment in the construction sector as a result of uncertainty surrounding Brexit, and a marked slowdown in demand from automotive.

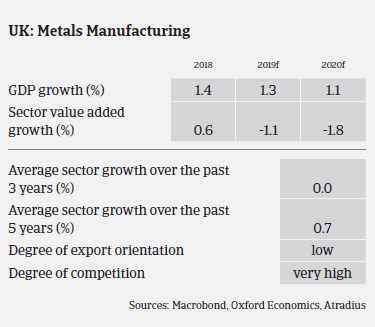

Additionally, energy costs remain an issue, as British steel producers pay 50% and 110% more for energy (electricity) than their German and French peers - even after compensation and exemption schemes provided by the government. This is a major competitive disadvantage domestically and internationally. At the same time, businesses suffer from higher commodity costs, lower sales prices for steel and fierce competition, both leading to an ongoing deterioration of profit margins. Steel value added growth is expected to level off in 2019 and to contract 1.0% in 2020.

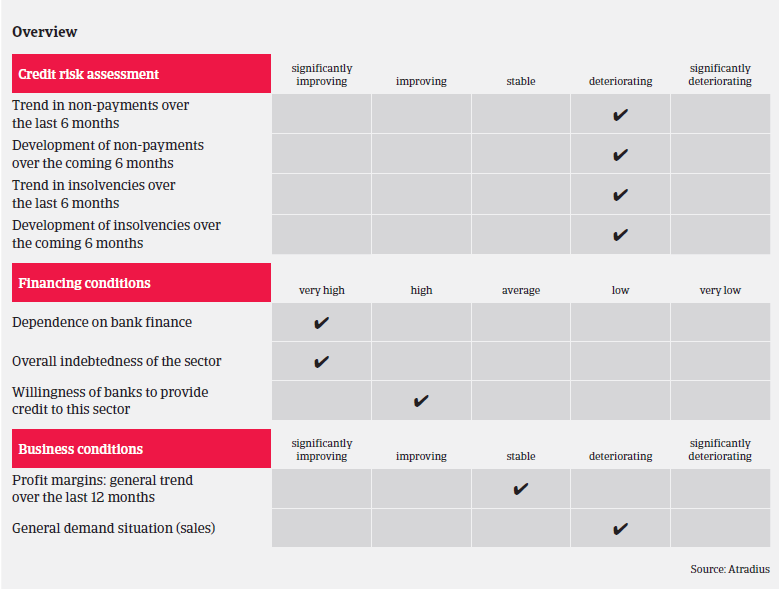

Historically service centres and steel stockholders already struggled to obtain decent margins against price volatility. Now the challenge is to maintain margins when falling prices are endemic. While banks are still generally willing to provide loans to the industry, lending conditions are increasingly getting tighter.

Regarding consolidation of steel producers, the Tata and ThyssenKrupp merger is off the table as competition authorities have blocked the deal. However, we observe that larger mills have increased their interest in acquiring more downstream businesses in order to support vertical integration. The main driver is to improve efficiencies and economies of scale, as well as increasing the bargaining power with major end-suppliers. This could potentially put pressure on independent service centres, as stockists associated with mills will receive preferential prices for their products.

The issue of sales price decline was exacerbated by Brexit-related stock piling, as more stock was accumulated in Q1 of 2019, ahead of the previous March 29th Brexit deadline. After the extension of the deadline, the stock was dumped on the market.

The ongoing uncertainty related to Brexit remains a major problem, especially if the EU and the UK fail to reach a comprehensive agreement on the post Brexit EU-UK trade relationship or if there is a hard Brexit. Potentially, British steel and metals exports could become subject to EU measures put in place to protect domestic steel. At the same time, with no preferential tariffs or simply no tariffs at all on non-EU trade, the UK and its metals and steel industry could become more vulnerable to cheap imports from Asia and the Middle East.

That said, it seems that many metals and steel businesses have made some contingency planning, including stock piling, to ensure they have suppliers from outside the EU, or setting-up a subsidiary in the EU to facilitate trade between the EU and a UK entity.

The average payment duration in the UK steel and metals industry is about 60 days. Due to squeezed margins in many businesses, payment delays have increased in H1 of 2019, and are expected to rise further in the coming 12 months. There have been three large metals and steel business failures recently, mainly the result of poor management decisions and the inability or unwillingness to adapt to the changing market environment. Insolvencies in the metals and steel industry are expected to increase about 5% in 2020.

Due to the recent business failures of some larger companies, and the subdued insolvency outlook for 2020, we have tightened our underwriting stance for metals and steel. While financial analysis remains a key part of the decision-making process, understanding the strategic plans of businesses is just as important. Other important criteria are succession planning and pensions, as some businesses are not generating the cash/profits to fund additional payments into their pension schemes.

Documenti collegati

1.06MB PDF